As a former hedge fund analyst and finance major, turned SAHM and blogger, I write a regular Family Financial Savvy series because I believe there is power and freedom in being financially literate… and sadly, it is a skill too many families lack. The most common issue families come to me with is wanting to pay down debt. This is a great financial objective, and with rising student loan balances, one almost every family struggles with. The key is to be smart about it – and it starts with figuring out which debt to pay off first.

Improving Your Family’s Finances

In the US, total household debt totaled nearly $13 trillion as of June 2017. This is comprised of mortgage debt, auto loans, student loans, and credit card debt. Surprisingly, credit cards actually make up the smallest portion of it.

Related post: The Ugly Truth About Student Loans

To improve your family’s finances, the first step is having a complete understanding of your family’s financial situation.

What is your total debt outstanding?

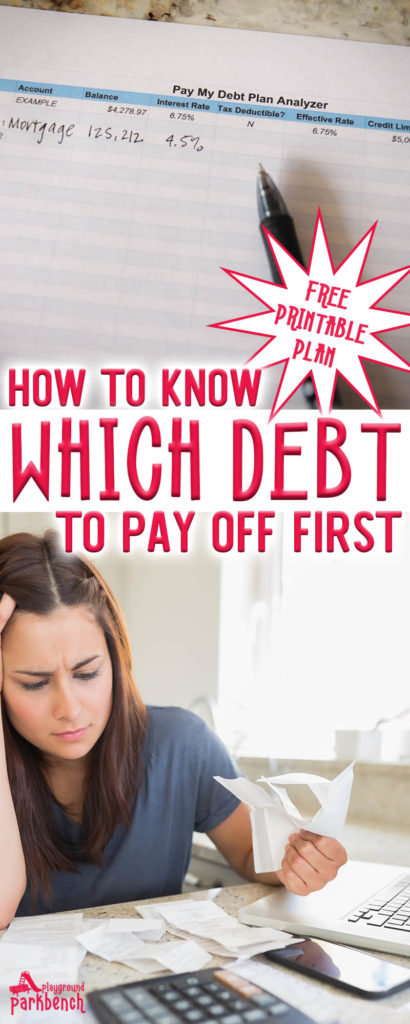

To understand your family’s financial situation, you need to know exactly how much debt you have outstanding. You can use my FREE Pay My Debt Plan Printable spreadsheet to figure this out. You can print out a PDF version, or, I highly encourage you to save a copy of the linked spreadsheet file to make the outlined steps below to figuring out which debt to pay off first easier.

Write down every single account you have outstanding – all your student loans, mortgages, car payments, credit cards, any payment plans with doctor and any other balances you carry.

Next, comes the most important part in determining which debt to pay off first. There is a tendency to want to paydown debt that requires the largest monthly payment or has the largest balance first… but that is often a mistake.

You actually want to paydown debt with the highest cost, or highest interest rate, first. Why? Because on a dollar for dollar basis, it is costing you the most to carry that balance.

You also want to pay attention to the after-tax cost of your debt. Mortgage and student loan interest payments may be tax deductible (see the changes in the new tax bill most likely to affect your family), leading to an even lower after-tax cost. If your mortgage or student loan interest is tax deductible, you can determine the after-tax cost by multiplying the interest rate on the debt by (1 less your marginal tax rate).

Be sure to write-in the interest rate and after-tax interest rates, as well as any credit availability to each of your debt accounts outstanding listed in your spreadsheet.

Which Debt to Pay Off First

Once you have filled out your spreadsheet with all your outstanding debt balances, you will want to sort your table by the Effective Rate column to determine which debt to pay off first. You should aim to pay off debt with the highest effective interest rate as quickly as possible, while maintaining minimum payments on all your balances so as not to increase rates or damage your credit history.

In the example above, you would want to pay off the credit card balance with a 9% interest rate first, followed by Student Loan 1.

Additional Strategies for Consolidating and Paying Off Debt

If you have low-cost debt with credit availability (like a mortgage or limited time 0% interest rate credit card), it may be worthwhile to use that availability to pay off high-cost debt immediately in one lump sum.

Most mortgages will allow you to mortgage up to 80% of the market value of your home. As you pay down your mortgage (or as home values rise), you may earn credit availability with your home mortgage. You can use this to take out home equity loans or refinance your home and take out cash to pay down high-cost debt more aggressively.

In the example above, you have significant credit availability through your mortgage. It is worth considering refinancing your home to access some of that availability, and use it to pay off all of the other higher cost debt you have outstanding. This leaves you with one single, lower cost, debt payment monthly.

If you do not currently have a mortgage or a mortgage with any credit availability, analyze your existing credit availability on current accounts or explore consolidating credit card balances on a single, lower cost credit card. Often times accounts with individual retailers carry much higher interest rates that general purpose credit cards. If you do choose to consolidate on a lower cost credit card, be aware of limited-time low rate offers, and be sure to pay off as much debt as you can before those rates increase.

__________________

What is your family’s most pressing financial concern now? How about five years from now? For more Family Financial Savvy, be sure to subscribe to Meghan’s weekly newsletter, join her private Facebook group: Family Finance Tips for Savvy Mamas, or follow her Family Financial Savvy board on Pinterest.

Love it? PIN THIS!

Meghan is a former hedge fund analyst and finance major turned stay at home mom to three kids, ages 6, 4 and 2. She shares kids learning activities, practical parenting tips and family financial savvy on her blog, Playground Parkbench. Join her private group, Family Finance Tips for Savvy Mamas to ask your questions and get more financial savvy made simple. You can catch her monthly in her virtual book club, Mom’s Book Nook, weekly via her newsletter, PGPB Weekly, or daily over on Instagram.

Meghan is a former hedge fund analyst and finance major turned stay at home mom to three kids, ages 6, 4 and 2. She shares kids learning activities, practical parenting tips and family financial savvy on her blog, Playground Parkbench. Join her private group, Family Finance Tips for Savvy Mamas to ask your questions and get more financial savvy made simple. You can catch her monthly in her virtual book club, Mom’s Book Nook, weekly via her newsletter, PGPB Weekly, or daily over on Instagram.

Melinda J Mitchell says

Katelyn, thanks for having Meghan guest!

Thanks, Meghan for the info and the spreadsheet. I will be using it!

Frank Langer says

Thanks for the helpful advice! Tackling debt can feel overwhelming, and your insights on prioritizing which debts to pay off first make so much sense. The idea of focusing on high-interest debts and creating a plan is really practical. Excited to start implementing these tips and work towards a debt-free future. Grateful for the guidance! 💸👍